The outlook for growth, trade and exporters

The global economy has once again proven more resilient than many expected. Despite the disruption caused by the war in Iran, higher energy prices and ongoing trade tensions, growth continues across most major markets—even as the pace moderates.

In EDC Economics’ summer 2026 Global Economic Outlook, our economists examine how elevated energy prices, geopolitical uncertainty and renewed tariff threats are reshaping the outlook for global growth, inflation and trade. While businesses have adapted to repeated shocks in recent years, resilience is beginning to show signs of strain as higher costs weigh on consumers, investment and international commerce.

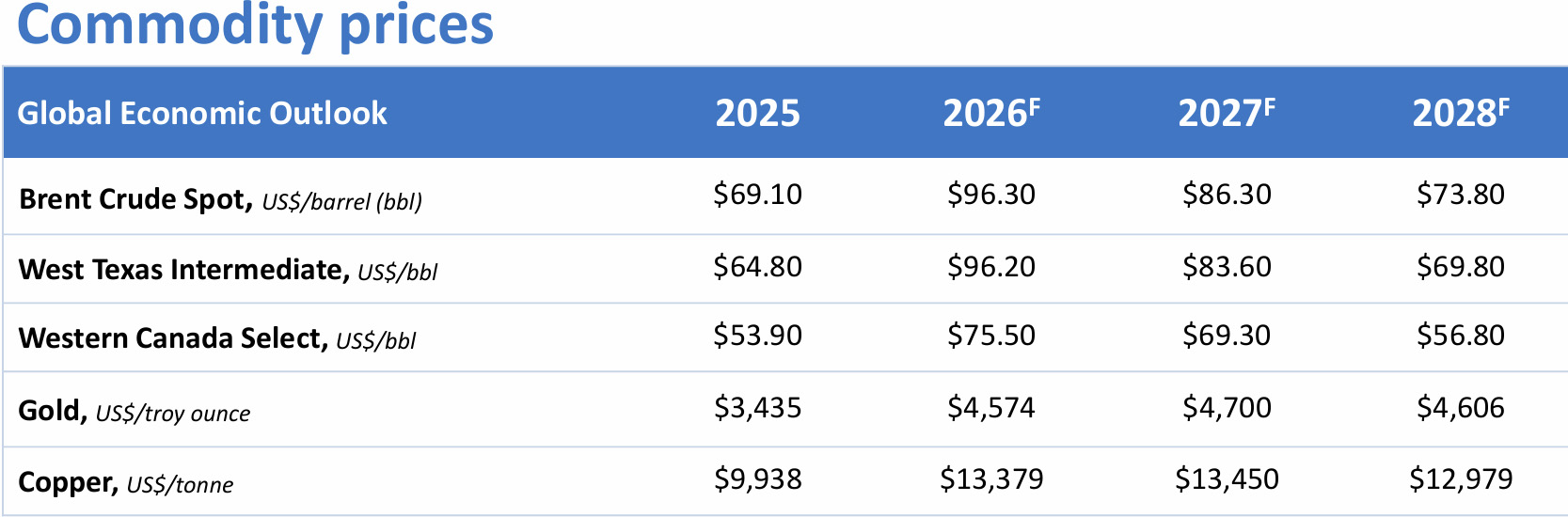

Key insight: The closure of the Strait of Hormuz temporarily disrupted roughly one-fifth of global traded energy supplies, driving prices higher and creating new uncertainty for businesses operating in global markets.

What’s in the summer outlook?

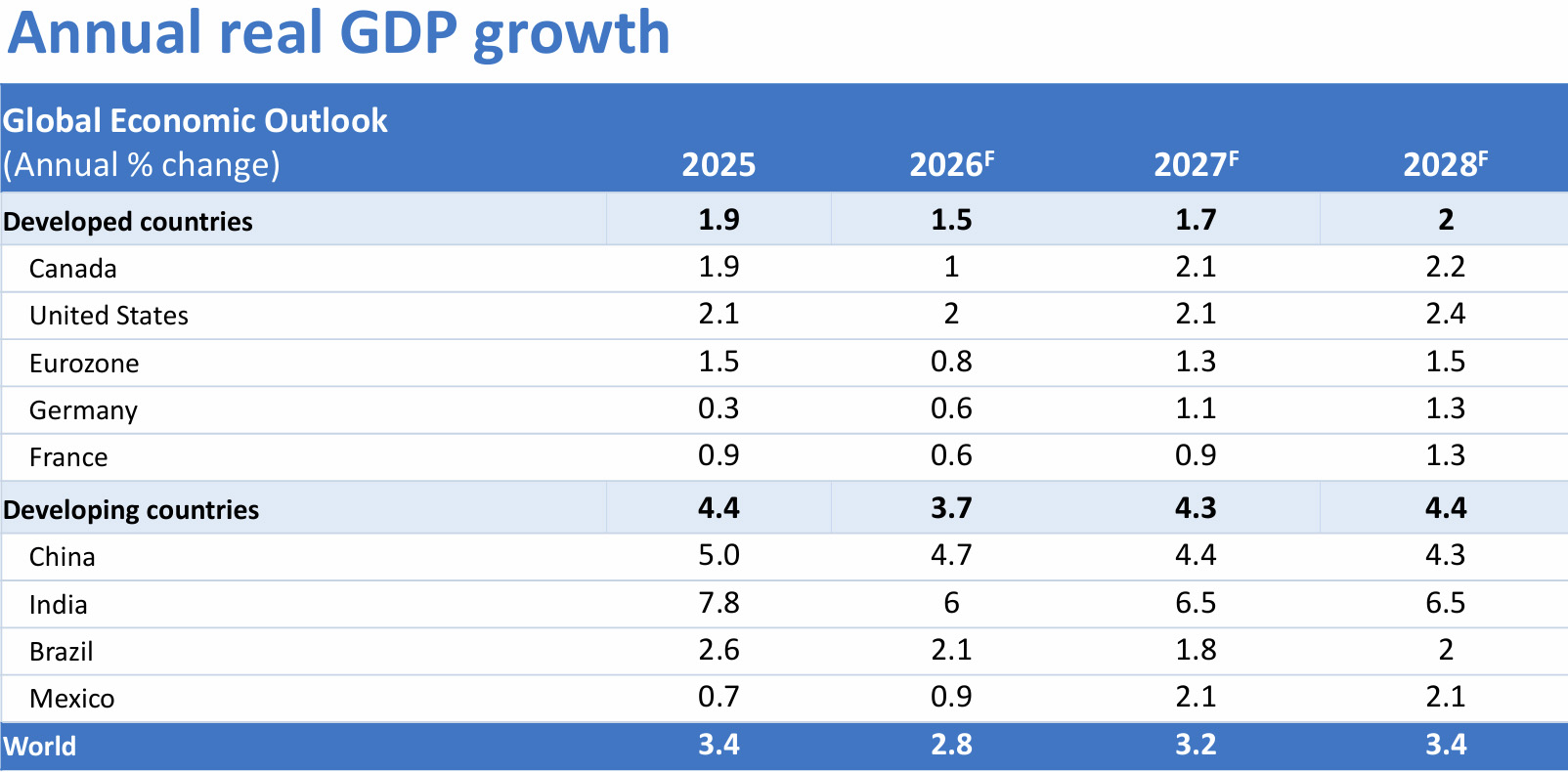

- Global growth slows, but remains resilient: The world economy continues to absorb major shocks, though growth is expected to moderate in 2026 before improving in 2027.

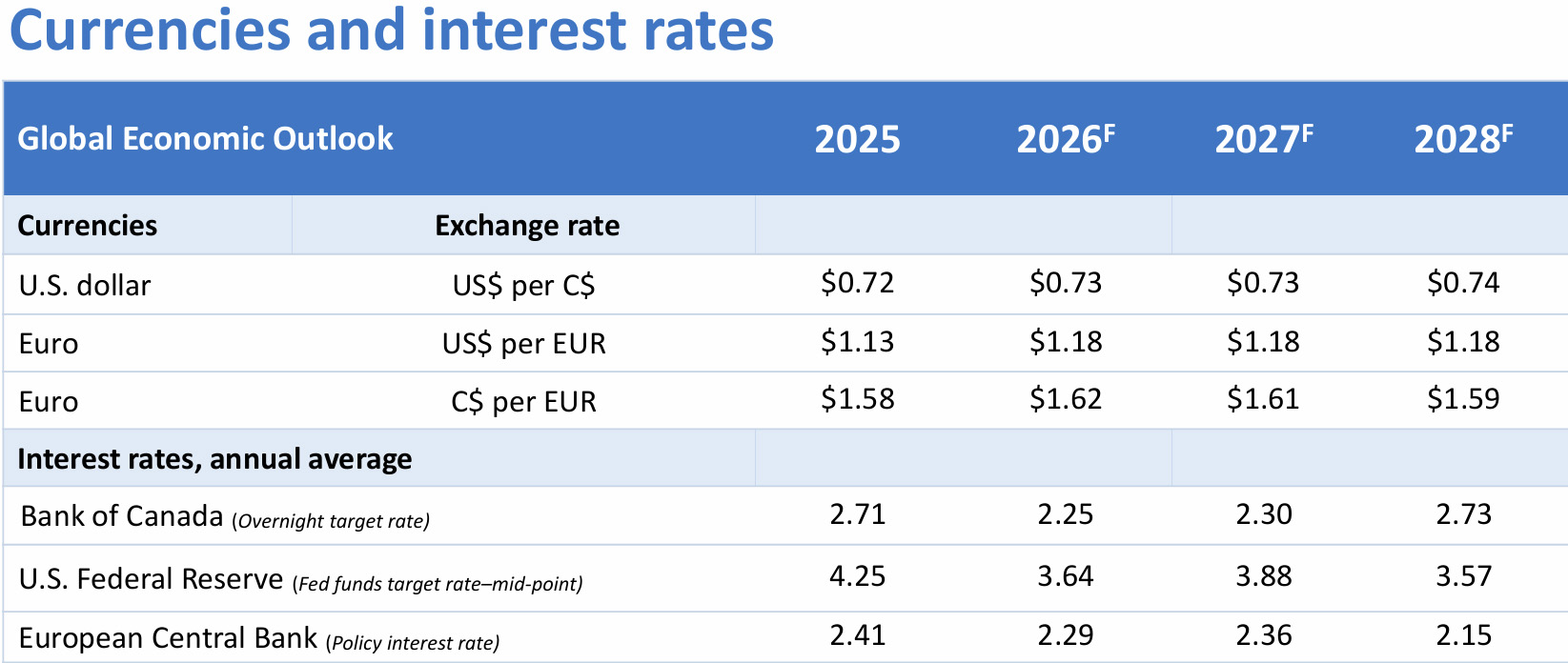

- Energy prices reshape the outlook: Higher oil prices are fuelling inflation pressures, complicating interest rate decisions and increasing costs for businesses worldwide.

- United States: Strong consumer spending and continued investment help support growth, despite trade tensions and weaker confidence.

- Canada: Exporters continue to face tariff uncertainty, weak business investment and cautious consumer spending, while higher oil prices provide support for energy-producing regions.

- Europe: Elevated energy costs and weaker external demand create challenges for major economies, including Germany and France.

- China: Exports continue to support growth as policymakers navigate weak domestic demand and ongoing trade frictions.

- Commodities: Updated outlooks for oil, gold and copper highlight evolving opportunities and risks for Canadian exporters.

Why it matters for Canadian exporters

Energy costs, tariff uncertainty and geopolitical developments continue to influence market conditions around the world. Understanding how these forces are affecting major economies, commodity markets and trade flows can help Canadian exporters identify opportunities, plan for risk and make more informed business decisions.

Who should download this report?

Canadian exporters, business leaders, trade professionals and market planners looking for forward-looking insights into global growth, key export markets, commodity trends and the economic forces shaping international trade.

Download EDC’s summer 2026 Global Economic Outlook for country forecasts, commodity outlooks and expert analysis on the trends driving global growth and trade in 2026 and 2027.