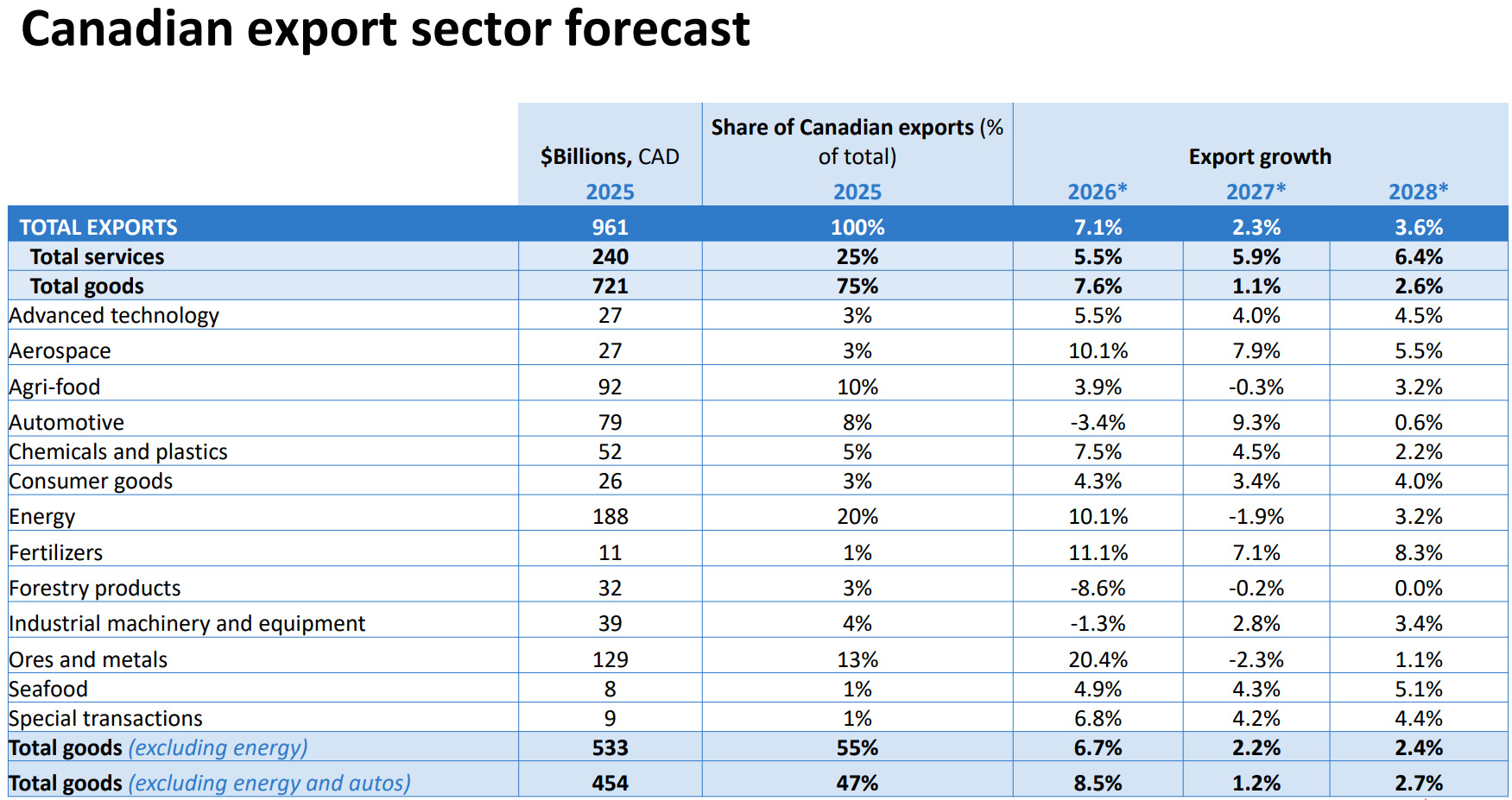

What’s in the spring forecast?

- Energy: Surging prices, driven by the closure of the Strait of Hormuz, and infrastructure investments are fueling growth for this sector, which represents roughly 20% of Canada’s goods exports. Exports are expected to increase by 10.1% in 2026 before falling by 1.9% in 2027 as global prices slip.

- Ores and metals: The price of gold is soaring, along with global commodity prices for copper and other metals. Ores and metals exports are forecast to grow by 20.4% in 2026 and then drop by 2.3% in 2027 as prices cool.

- Agri-food: Lower Chinese tariffs and strong harvests that boosted inventories of several commodities have improved the outlook for this key sector in 2026. While weather risks, including a potential shift toward El Niño conditions, remain a uncertainty, exports are expected to increase by 3.9% in 2026 before a slight decline of 0.3% in 2027.

- Autos and parts: With U.S. sectoral tariffs still in place, the auto sector will face significant headwinds in 2026. Canadian automotive exports are forecast to decline by 3.4% in 2026. Previously announced production plans and new models should support a modest recovery in 2027, with exports increasing by 9.3%.

- Services: Services exports are expected to grow robustly, led by technology-related commercial services and major tourism events, such as the 2026 FIFA World Cup. After moderating in 2025, services growth is expected to pick up to 5.5% in 2026 and 5.9% in 2027.

- Other sectors: The full report explores opportunities and challenges for Canada’s fertilizers, chemicals and plastics, aerospace, forestry products and advanced technology sectors.

The bottom line

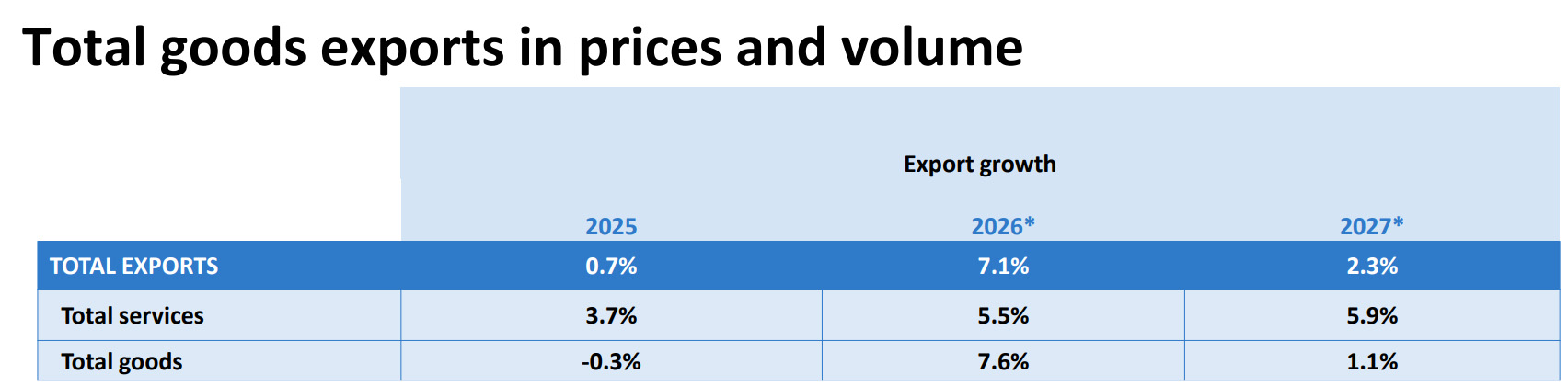

Like much of the world, Canada’s export outlook will be shaped by the Gulf conflict and the Strait of Hormuz disruption. While the benefits to Canada’s headline exports—and to some sectors—could be significant, they would come largely through higher prices. The longer the disruption persists, the higher global fuel, fertilizer and freight costs will rise, and the tighter financial conditions may become—raising risks to exports and to our forecast. Canadian exporters’ continued ability to navigate this uncertainty will be important to sustaining the export momentum that kicked off 2026.

Who should download this report?

Canadian exporters, trade professionals, manufacturers and globally focused businesses seeking insight into energy markets, geopolitical risk and global growth trends.

Download EDC’s Global Export Forecast for sector insights and analysis designed to help Canadian exporters navigate risk, trade and growth in a volatile global economy.

Read the full Global Export Forecast report (PDF)