EDC Economics looks back at an eventful year and the road ahead for 2020

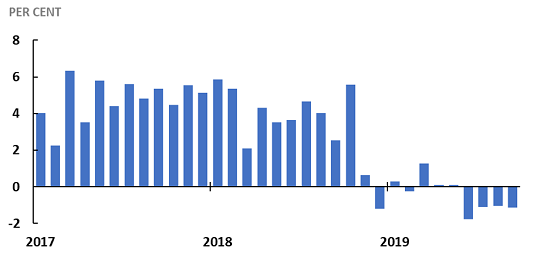

Global goods trade contracting

Source: CPB Netherlands

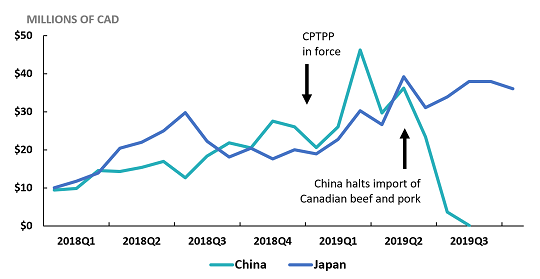

Canada’s agriculture exports caught in the crossfire

Source: Trade Data Online

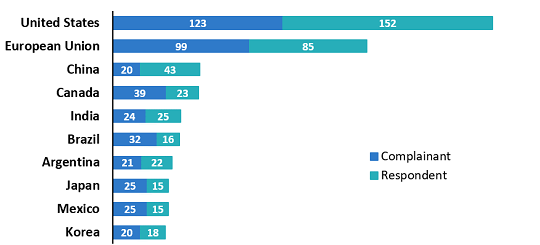

Uncertainty about the World Trade Organization’s dispute settlement system

Source: Peterson Institute for International Economics, WTO trade monitoring database

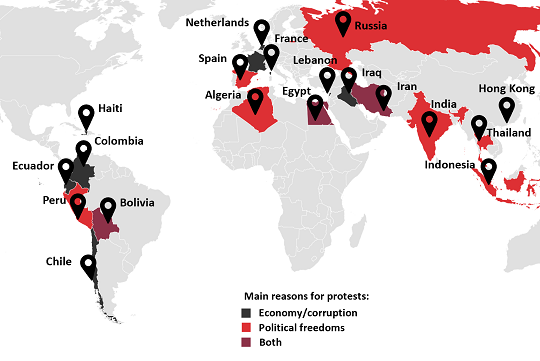

Global protests and social unrest

Source: GZERO media, EDC Economics

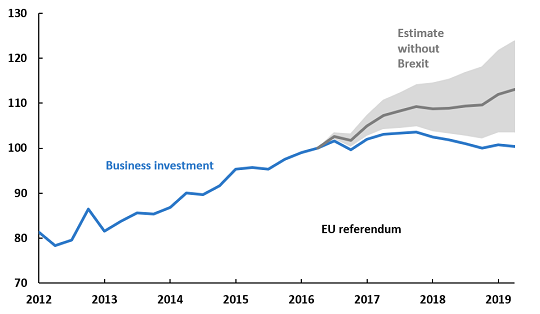

Brexit

Source: Bank of England, Monetary Policy Report, November 2019

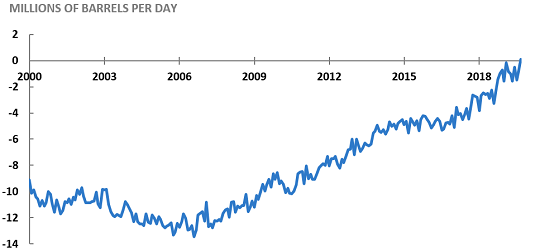

American oil dominance

Source: Energy Information Administration (EIA)

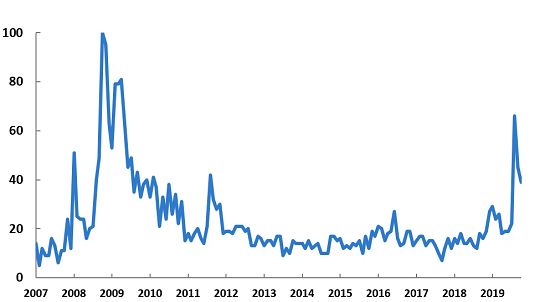

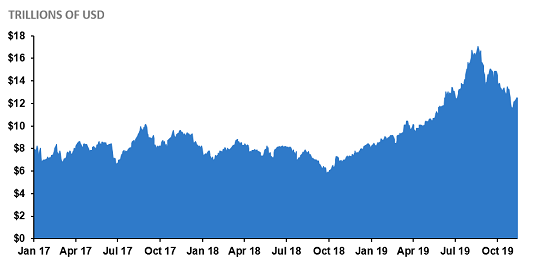

Recession worries

Source: Google Trends

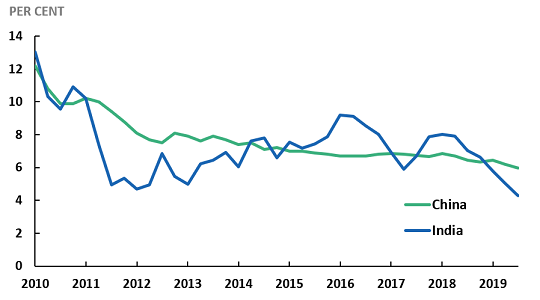

Emerging Asia slowdown

Source: Haver Analytics, EDC Economics

Widespread central bank interest rate cuts

Source: Bloomberg, EDC Economics

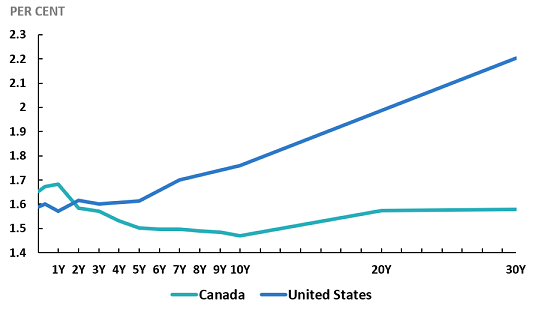

Canadian yield curve inversion

Source: Bloomberg, EDC Economics