The drive to diversify

Two-track Canadian trade in the 21st century

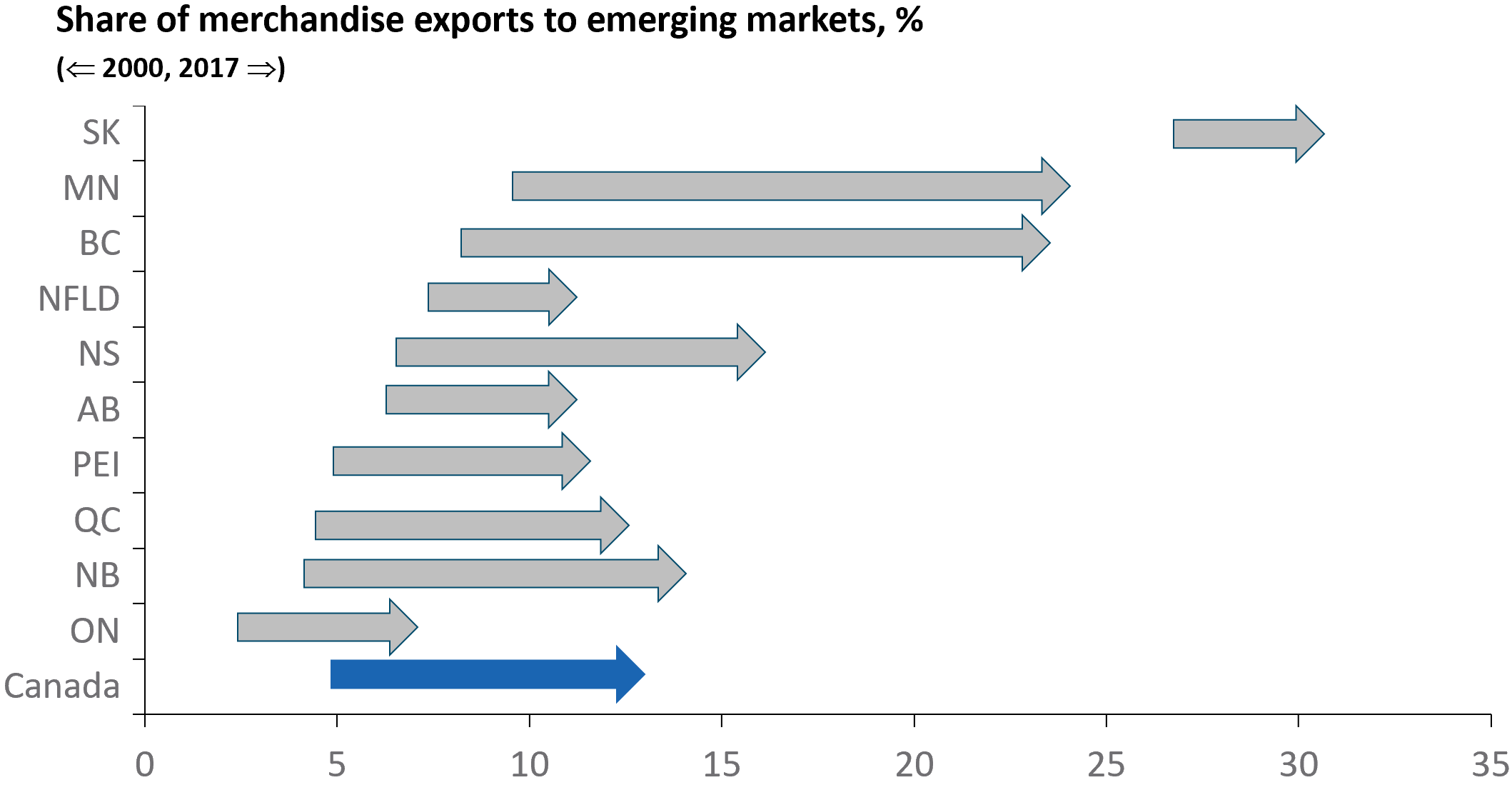

Provincial diversification

Sources: EDC Economics; Statistics Canada

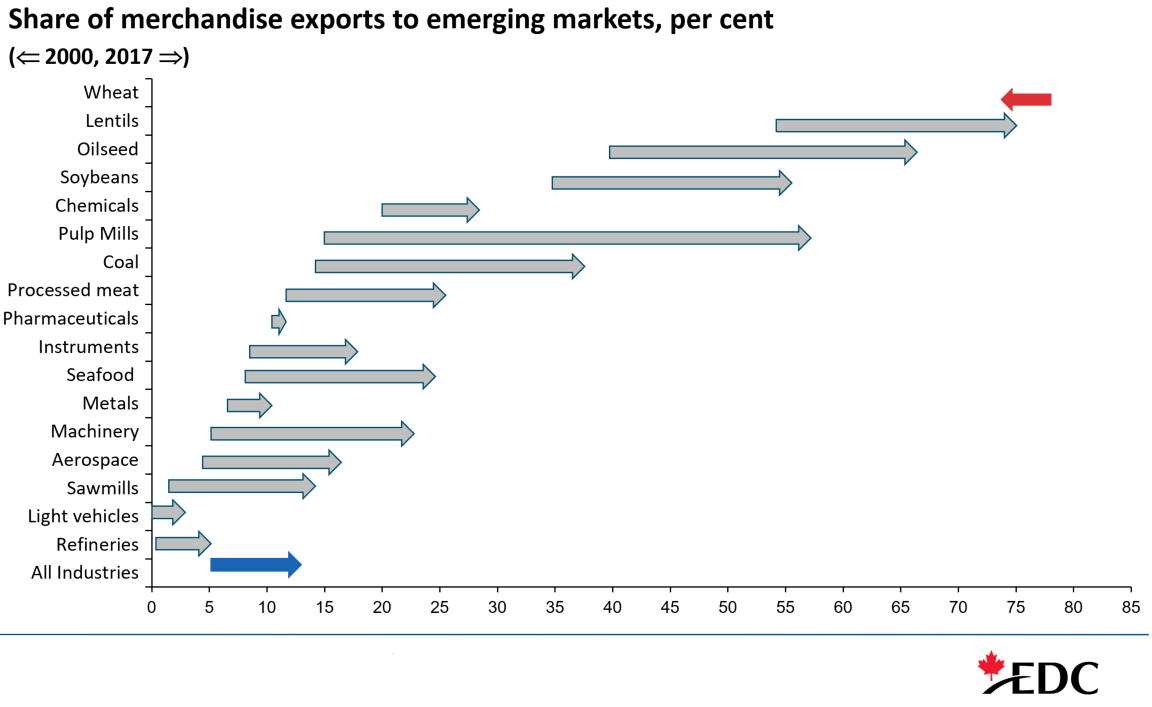

Product diversification

Sources: EDC Economics; Statistics Canada

The U.S. versus non-U.S. difference is reflected in shifts in how Canada’s trade is transported. The majority of Canada’s trade with the U.S. takes place by road and, to a lesser extent, rail. Not surprisingly given the weaker Canada-U.S. trade performance, the shares of these transportation modes have collectively fallen over time (from 70 to 60%).

Conversely, Canada’s trade with other markets, such as Europe and Asia, primarily uses marine and air modes. These shares have increased, up from almost one-quarter to one-third (24 to 31%, respectively; the residual category is largely pipelines, which has increased from 6 to 9% of the total. These results show that Canada’s merchandise trade has become more diversified over time.

But how do we compare with other OECD countries?

Export diversification among OECD countries

Export market concentration

Herfindahl-Hirschman Index, OECD countries, 2015

Sources: EDC Economics; World Bank

Services and investment more diversified than goods exports

We’ve examined goods trade, now let’s consider other forms of commerce, before turning to the future.

Most trade discussions start with Canada’s goods exports, as we did above. However, expanding the scope shows that Canada’s international trade in services depends less on the U.S. market than our goods exports. This story is similar for both inward and outward foreign direct investment, where less than half of the total activity now involves the U.S. market. Notice that for all these measures, the share of Canada’s total international commerce occurring with countries other than the U.S. has grown over time.

Sources: EDC Economics; Statistics Canada

Canadian companies looking to diversify

Looking ahead, one of the clearest findings from EDC’s recent Trade Confidence Index survey of 1,000 Canadian exporters is that, over the past six months, more Canadian companies have diversified their operations and are looking to do so in the future.

There was a significant increase in the share of Canadian exporters who have started exporting to new countries (44%, up from 31%, with increased international demand from a growing global economy being a main driver) and those who plan to export to new countries in the next two years (64%, up from 49%).

Source: EDC’s Trade Confidence Index

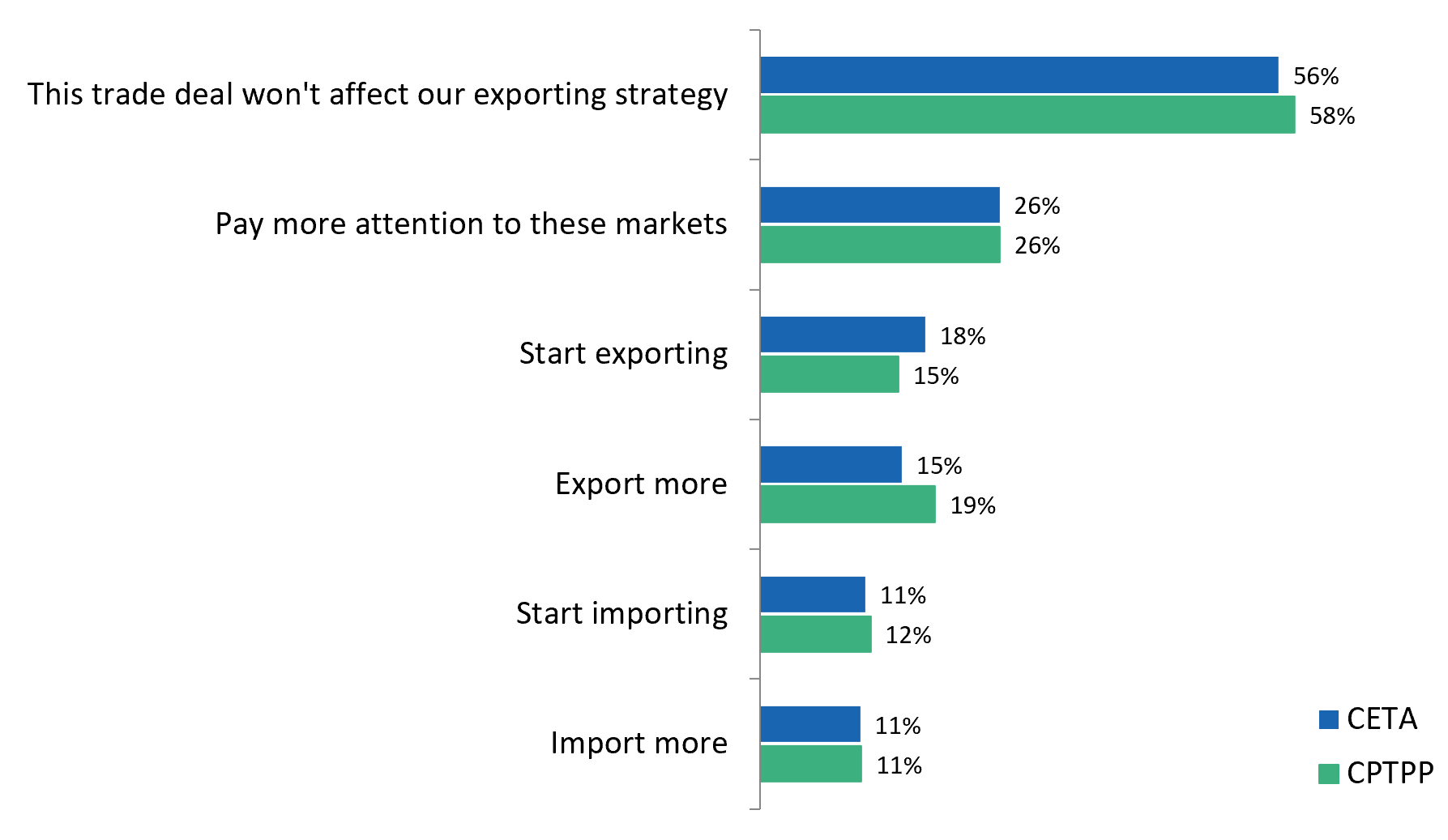

New trade agreements helping to fuel plans

Canada recently signed two major trade deals with countries in the European Union and Asia Pacific region (namely the Comprehensive Economic and Trade Agreement, CETA, and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, CPTPP). Just over one-quarter of Canadian exporters say they are now paying more attention to these markets, particularly Germany, France and Japan. Existing traders in these markets are looking to increase exports and imports, and many Canadian companies are looking to start exporting to, and importing from, these trade blocs.

Source: EDC’s Trade Confidence Index

Beyond export market diversification, there was also a significant increase in the share of Canadian exporters who report having investments outside of Canada (17%, from 11%), and those who plan to do so (22%, up from 12%), where for the latter the U.S. and China are key target markets for planned Canadian foreign direct investments. These trends have already begun, as shown by the robust growth in Canada’s outward foreign direct investments in recent years.