Why trade-enabling infrastructure matters for Canada

You should also check out

EDC Economics: Connecting Canada to the world

With timely insights and financial analysis from our experts, Export Development Canada can help you enter new markets, grow your global business, and reduce risks with confidence.

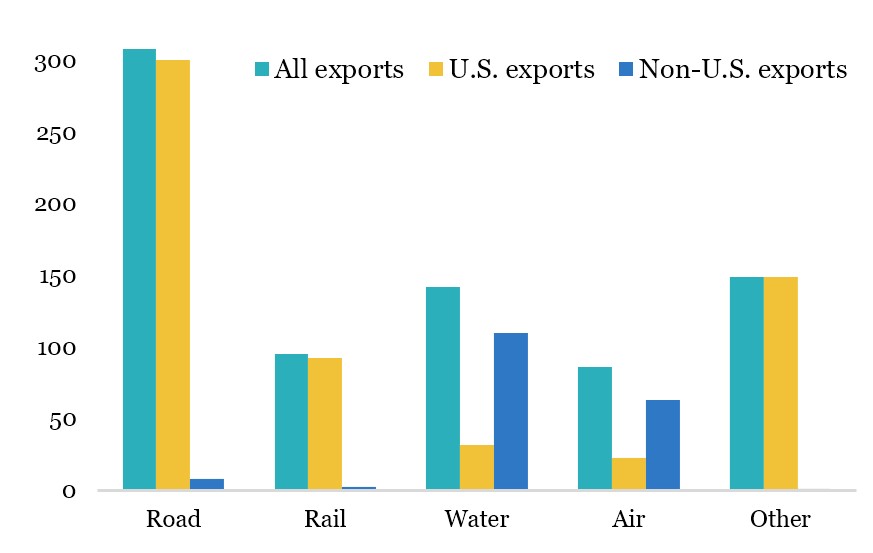

Share of Canadian exports by mode, C$ billions, 2024

This commentary is presented for informational purposes only. It’s not intended to be a comprehensive or detailed statement on any subject and no representations or warranties, express or implied, are made as to its accuracy, timeliness or completeness. Nothing in this commentary is intended to provide financial, legal, accounting or tax advice nor should it be relied upon. EDC nor the author is liable whatsoever for any loss or damage caused by, or resulting from, any use of or any inaccuracies, errors or omissions in the information provided.