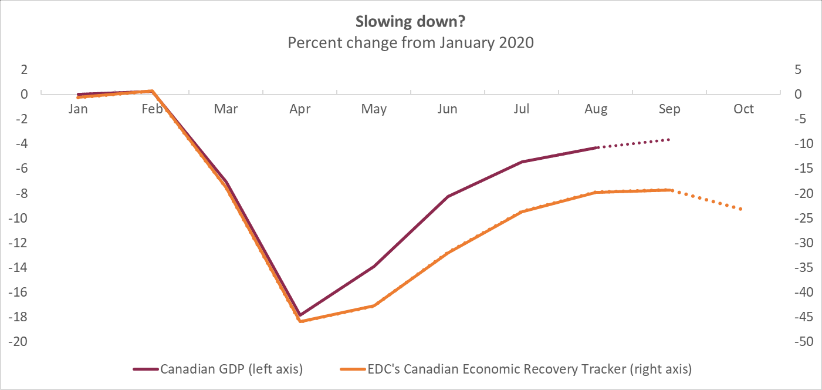

According to EDC’s Canadian Economic Recovery Tracker (CERT), Canada might be nearing a critical turning point in the third economic phase of this global pandemic.

The first phase, in March and April, featured a sudden stop in economic activity, and a major shift to working and shopping online. This period was marked by the initial spike of COVID-19 cases and widespread government restrictions imposed across much of the world, to contain the virus. With many businesses shutdown and people largely confined to their homes, economic activity plummeted at the fastest rate ever recorded. With personal mobility limited and people fearful of contacting the virus, there was also a rapid shift toward a more digital world.

The second phase was the reopening rebound, which occurred over the summer. Unprecedented government support was coming through for households and businesses, and as the first wave of the virus came under control, lockdowns were eased. Some businesses reopened physical locations (often at reduced capacities) to complement their virtual storefronts. As we learned more about the virus, hygiene improved and mask wearing became common, which allowed for safer in-person commercial interactions. Consumers ventured out of their houses, increasing mobility. Now past their initial pandemic shock, people started adjusting, creating new routines, and making purchases they delayed during lockdowns. The economic rebound was sharp—much faster than most expected—but only partial.

As predicted in EDC’s Global Economic Outlook, “fast didn’t last.” Now Canada is in a third, slower growth recovery phase, with a long, uncertain and highly uneven situation across sectors. In September, a second wave of COVID-19 cases in Canada began to accelerate. Some health restrictions were reimposed, but unlike the first wave response, they’ll likely do less economic damage for two reasons. First, they’re much more targeted to specific hotspots and activities. Second, we’re not starting to socially distance, we’re continuing to do it. Since we’ve been through this drill before, another economic sudden stop is unlikely. Many are adapting to “business as unusual.” A fortunate 2.4 million Canadians, who didn’t previously do so, are working from home because of the pandemic.

The key question now isn’t whether growth will slow; it already has. Instead it’s whether growth will stall completely and turn negative? Indeed, several forecasters expect negative growth in Europe in the fourth quarter in countries where the strictest lockdowns are being reimposed. The Bank of Canada now puts Canada’s growth at under 1% at annual rates in Q4.