EDC COVID-19 impact survey suggests the worst is behind us

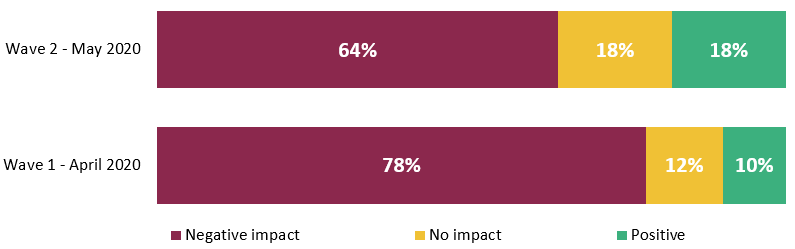

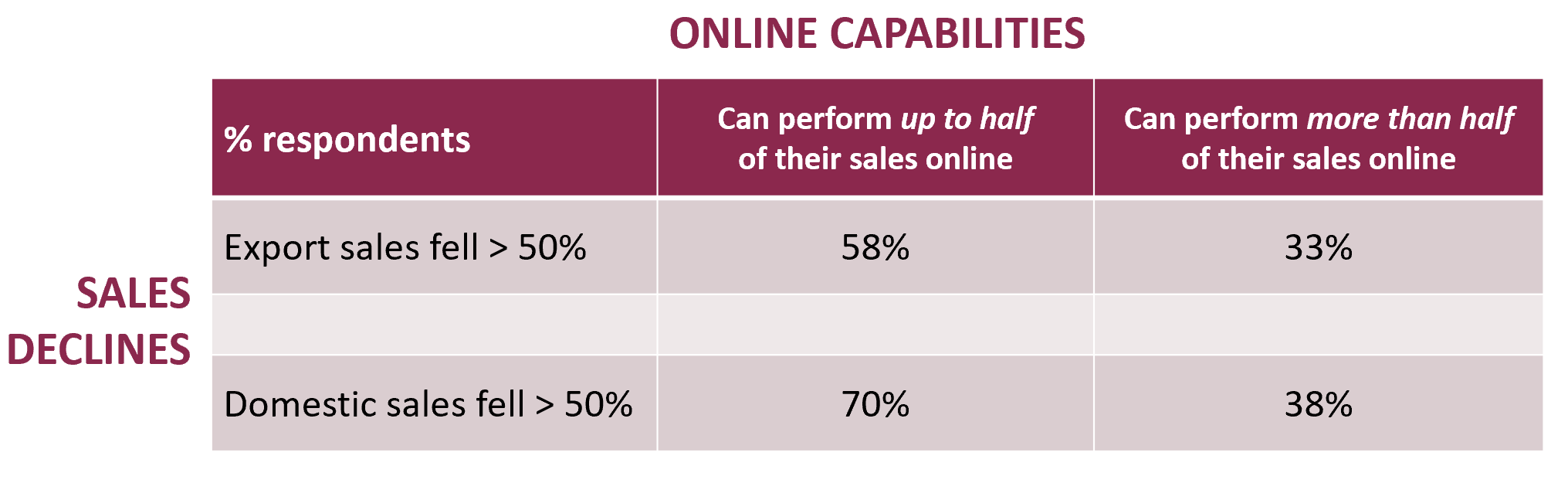

Domestic sales

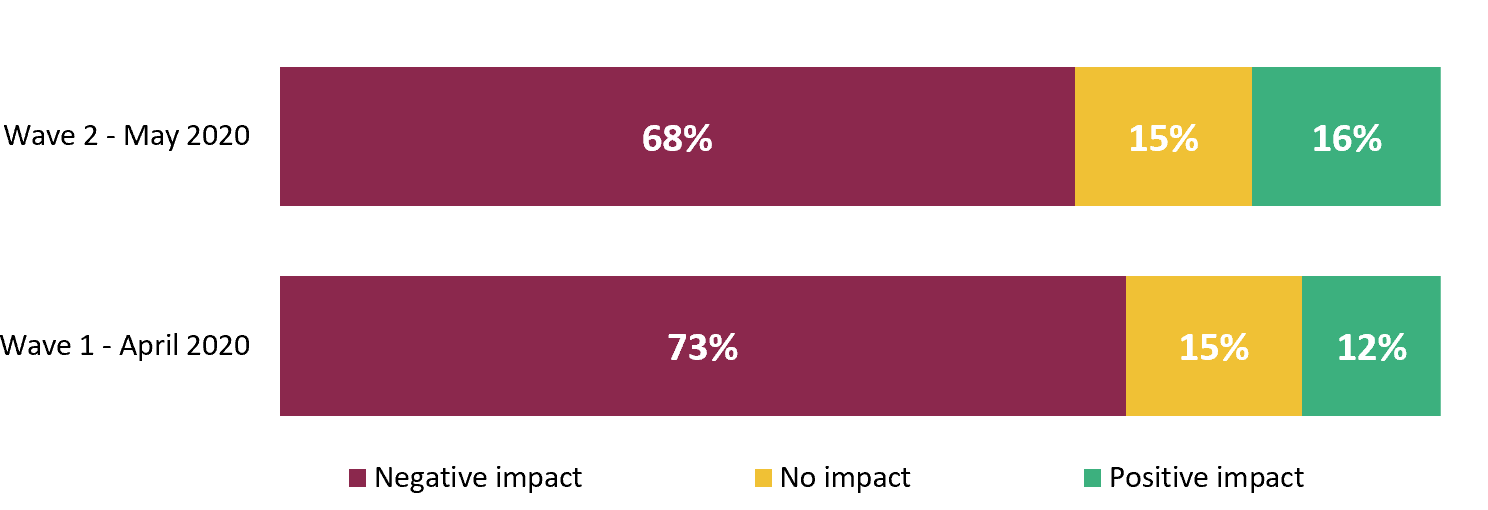

Export sales

Authors

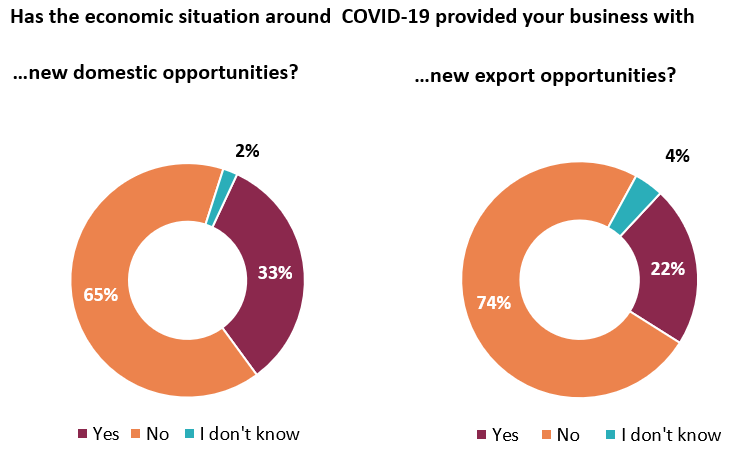

Domestic sales

Export sales

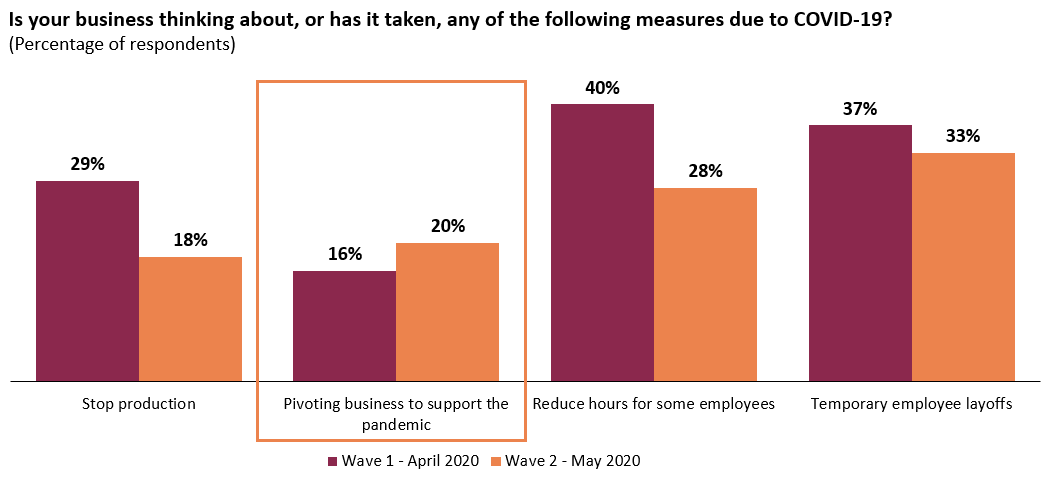

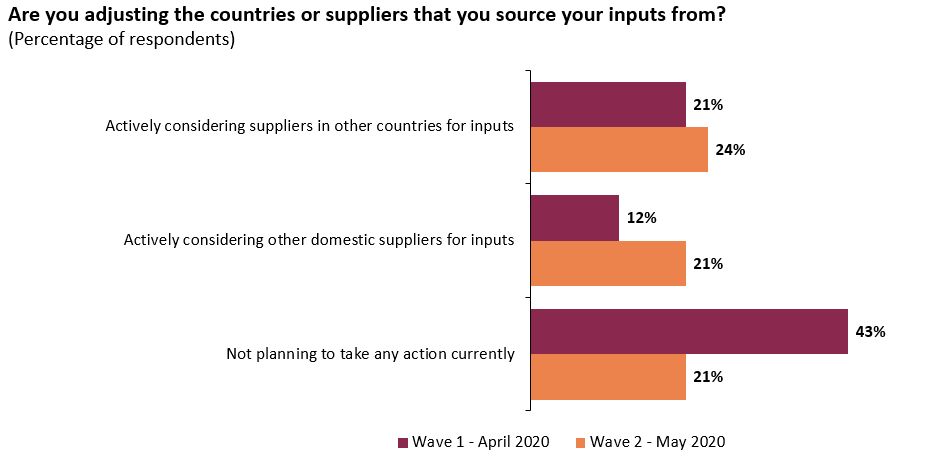

The EDC Research Panel’s January survey highlights the challenges imposed by the global pandemic.

Rising defence spending is creating new export opportunities for Canadian firms.

Rising energy prices and trade tensions are reshaping the global economic outlook. Explore what it means for growth, trade and Canadian exporters.

Keep track of the international markets that matter to your business. Get the latest financial and macroeconomic information for both developed and emerging markets.

Prepare for tariffs and strengthen contracts and supply chains amid CUSMA changes.

Where Canadian mining firms face risk and opportunity in Latin America’s mining sector