How you can take advantage of the Canada-EU trade relationship

A big deal

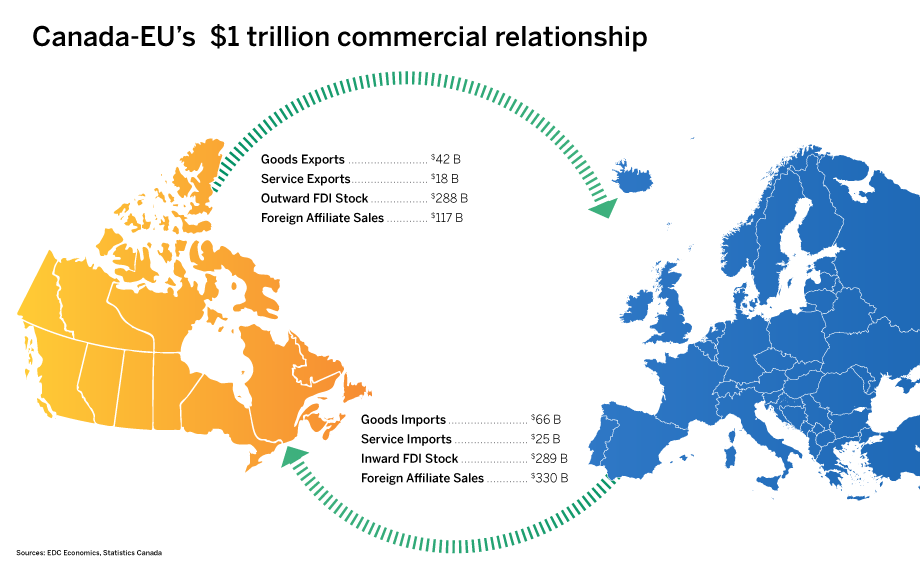

This is one of Canada’s most ambitious trade agreements, and it’s not just about tariffs. While it established 21st century standards for trade in goods, it also addressed services, non-tariff barriers, investment, government procurement, labour, the environment, and regulatory cooperation. CETA is also a big deal, covering one of Canada’s most important commercial relationships internationally — worth over a trillion dollars! The European Union is Canada’s second-largest trading partner, after the United States. It accounts for 30% of Canada’s international investment, 26% of foreign affiliate sales activities, and 11% of our two-way trade.