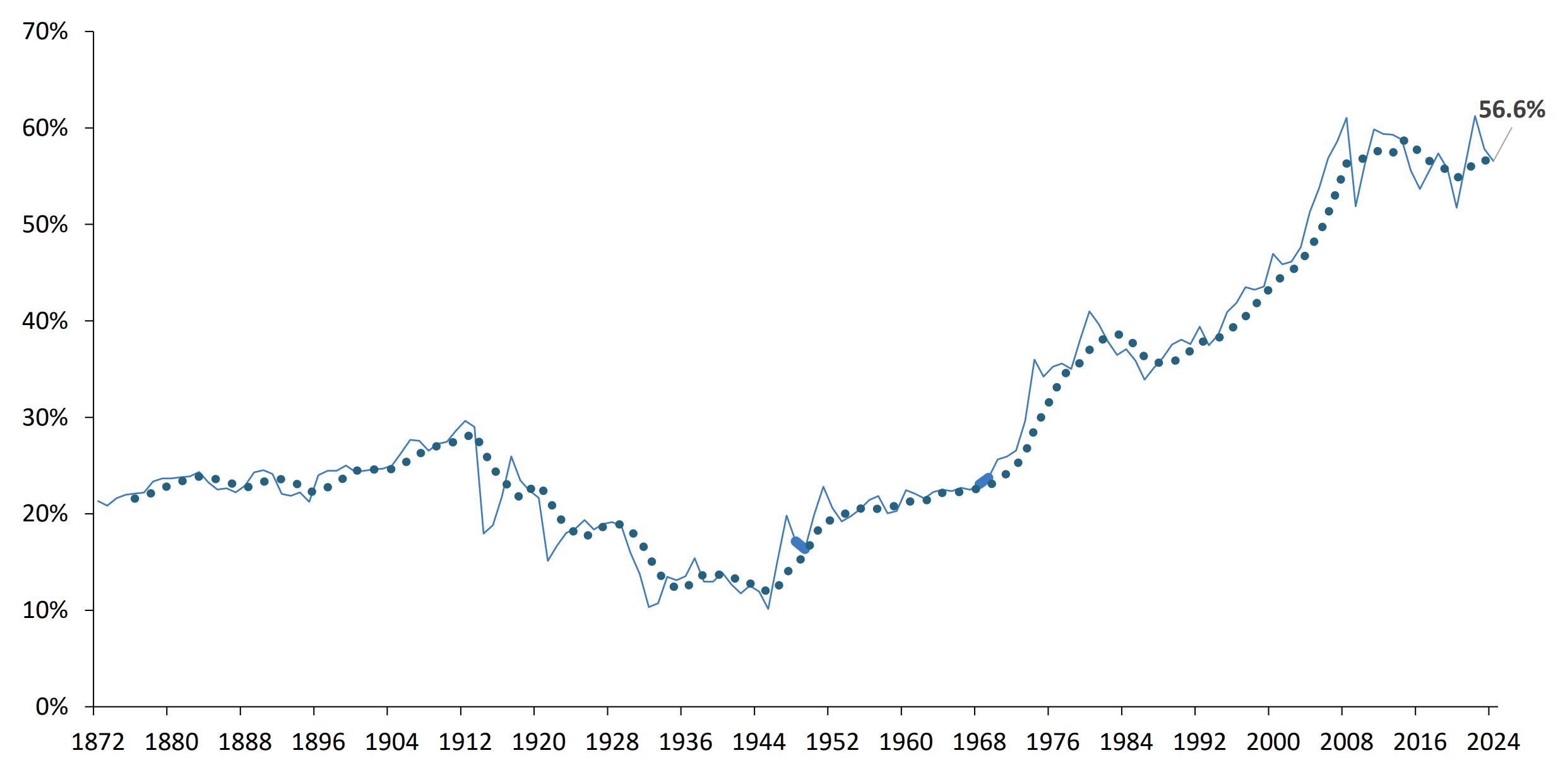

Since the global financial crisis in 2008, the share of global trade has been relatively stagnant. Initially, protectionist measures and trade policies increased worldwide as governments sought to protect key industries and constituencies during economic upheaval.

This trend continued through the first Trump administration and Brexit (the United Kingdom’s withdrawal from the European Union), which frayed long-standing trade relationships, and has accelerated since the new U.S. administration took office in early 2025. New U.S. tariffs and trade restrictions have prompted retaliatory actions from key trading partners, raising costs for businesses and disrupting supply chains. Two-thirds of global firms report tangible cost increases tied to trade policy uncertainty and duties.

The global pandemic further disrupted supply chains, causing costs to surge and inventories to run out, which intensified these trends. As a result, companies and governments have pursued strategies, like nearshoring, to build resilience in the face of uncertainty.

While the overall share of trade to global GDP is a key measure of globalization, other indicators can reveal how it’s changing. For example, the distance travelled by imported goods provides insight into the evolution of supply chains and global integration.

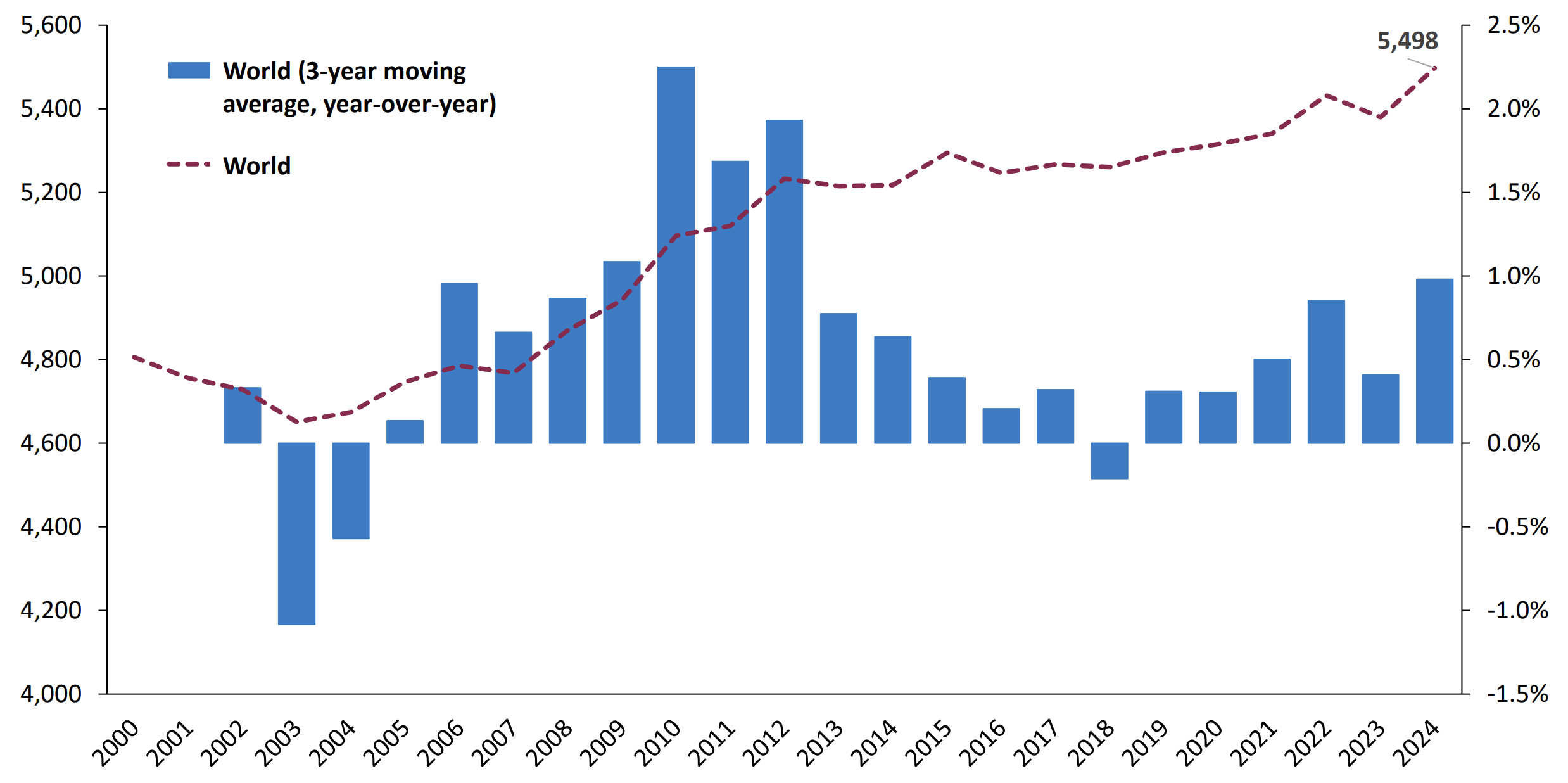

As Chart 2 shows, the trade-weighted average import distance has increased significantly since 2000. Although China joined the WTO in 2001, it took several years for the impact to echo through supply chains. Between 2003 and 2012, globalization accelerated as import distances increased rapidly. While China was a key player, other emerging economies—Vietnam, India, Brazil, Mexico, Peru, Chile, Malaysia and others—also played important roles.