One year later: How U.S. tariffs reshaped Canada-U.S. trade

How U.S. tariffs reshaped global trade and supply chains

Insights and analysis from EDC on navigating the U.S. business environment

Canada-U.S. trade impact: Why services helped offset tariffs

CUSMA and U.S. tariffs: Why compliance costs are rising

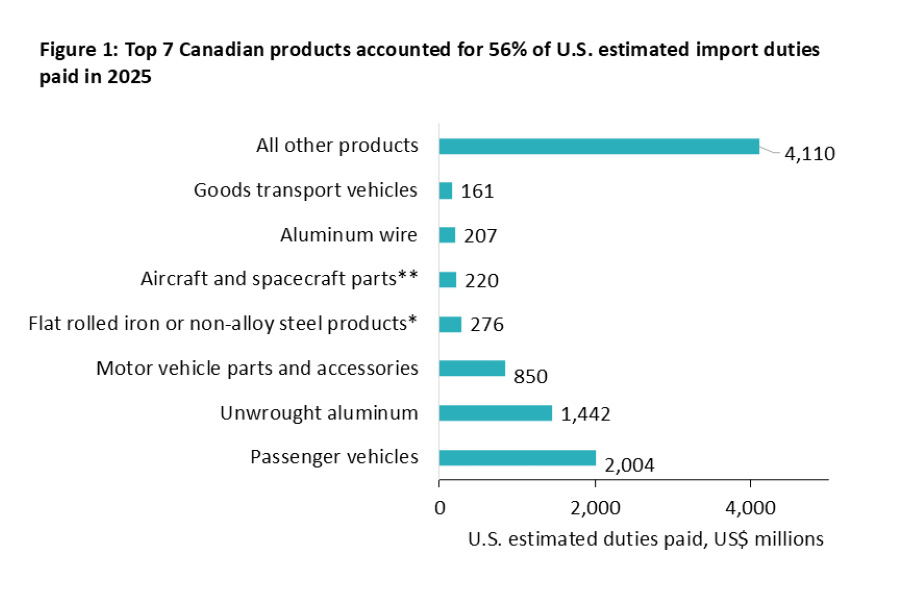

Where U.S. tariffs hit Canadian industries hardest

*Of a width of 600 mm or more, that are clad, plated, or coated.

**Includes parts for balloons and non-powered aircraft, powered aircraft and spacecraft and unmanned aircraft.

Sources: U.S. Census Bureau, EDC Economics

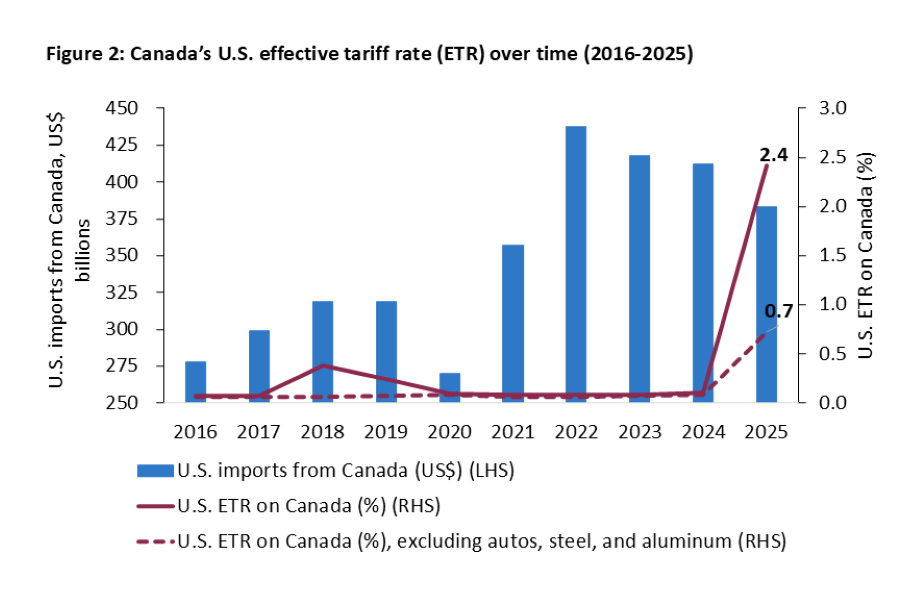

Notes: U.S. effective tariff rate (ETR) = estimated duties paid on U.S. goods imports from Country X as a share of total U.S. goods imports from Country X. To represent automotive, steel and aluminum products, given varying U.S. tariff implementation timelines; HS product additions/exclusions; and complexity in capturing full HS code coverage (including derivative products), the following HS codes were used for this illustrative analysis: HS 8703 Motor cars and vehicles for transporting persons, HS 8704 Motor vehicles for transport of goods, HS 8708 Parts and accessories for motor vehicles (8701-8705), HS 72 Iron and steel, HS 73 Articles of iron or steel and HS 76 Aluminum and articles thereof.

Sources: U.S. Census Bureau, EDC Economics

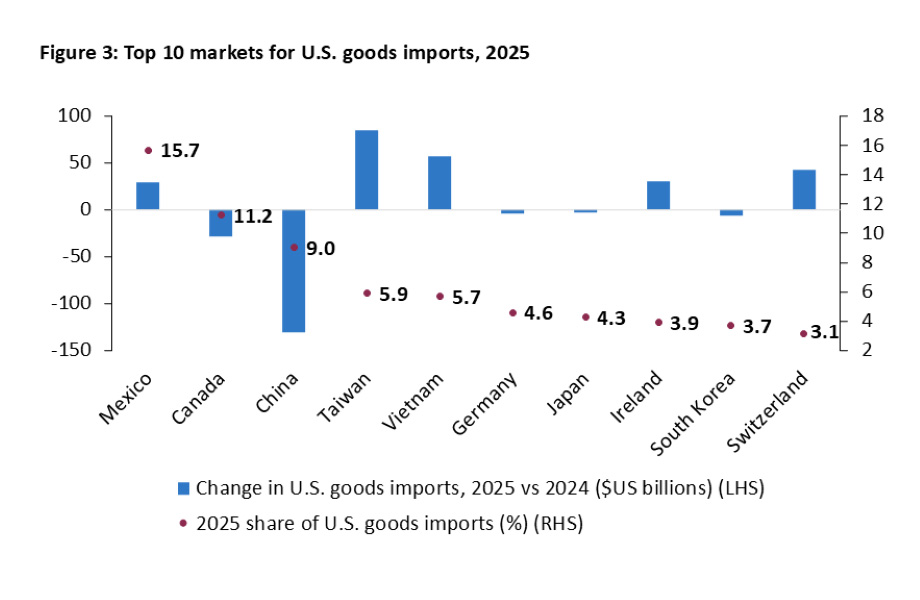

Note: These 10 countries accounted for two thirds of the U.S.’s 2025 goods imports.

Sources: U.S. Census Bureau, EDC Economics

Canadian manufacturing under pressure from U.S. tariffs

Slower momentum across the U.S, Canada and Mexico reflects softer spending and rising costs.