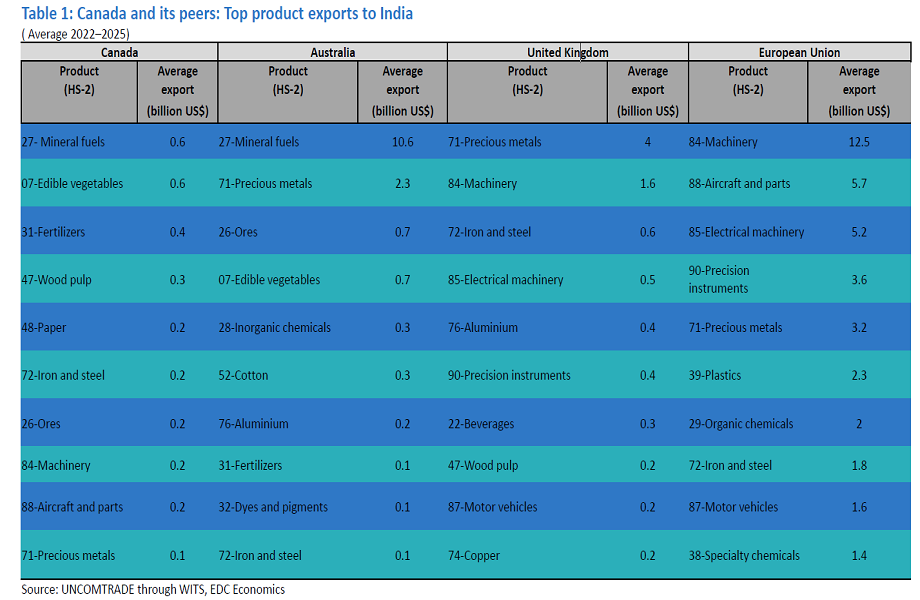

A common challenge for Canadian exporters in the Indian market is the high, complex and often unpredictable Indian tariff regime. According to the World Trade Organization (WTO), India’s average applied most-favoured-nation (MFN) tariff was 16.2% in 2024 and 36.7% for agricultural products.

Recent trade agreements with India aim to lower, or eliminate, tariffs on goods. Official announcements indicate that under the India–U.K. agreement, tariffs will be cut on about 90% of goods, with 85% becoming tariff-free within a decade. The India–Australia ECTA has eliminated tariffs on 85% of Australia’s goods exports, with another 5% to be phased out over the six years from entry into force. For the EU, reports suggest that close to 97% of goods will benefit from tariff cuts, or elimination, which will be phased in over a period of up to 10 years.

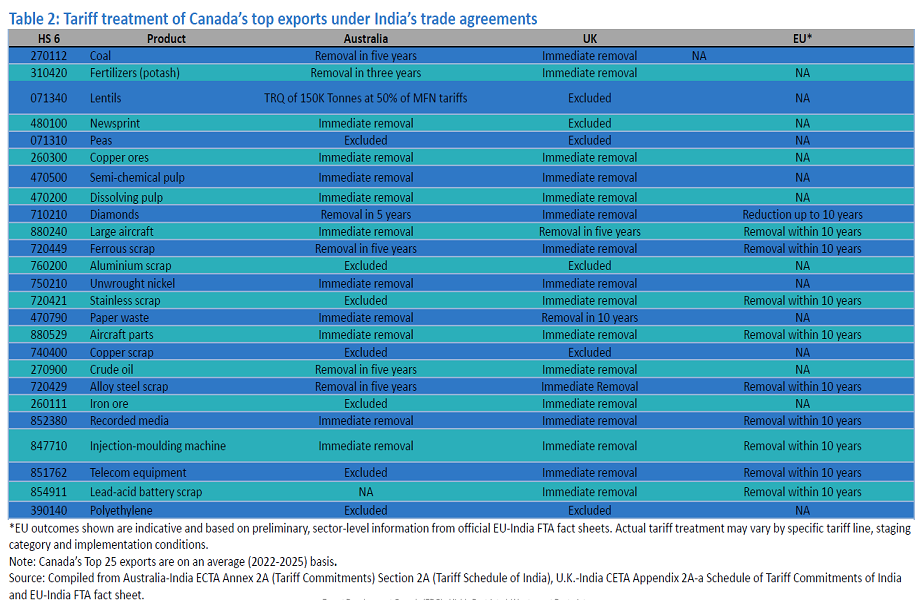

Although details vary by agreement, India continues to protect sensitive agricultural sectors such as dairy, meat (except sheep meat) and cereals. Agricultural gains are mainly in seafood (for Australia and the U.K.), processed agri‑foods, like bread, pastries and fruit juices, where tariffs are mostly removed or significantly reduced. Alcoholic beverages are subject to gradual tariff reductions rather than elimination. These cuts are meaningful given the very high starting tariff rates.

In non‑agricultural sectors—including machinery and electrical equipment, chemicals, pharmaceuticals, metals and minerals—tariff cuts are larger and happen faster. Transport equipment outcomes are more mixed: For the U.K. and Australia, aerospace gains are mostly limited to aircraft parts and components, while access for motor vehicles remains limited. For the EU, information suggests tariffs on finished aircraft will be gradually removed, while motor vehicles will get limited, quota-based access.

The trade agreements set out clear, internationally recognized rules to address food safety and animal and plant health requirements (sanitary and phytosanitary, or SPS), making regulations more transparent and helping exports move faster into India. They also encourage authorities to treat each other’s rules as “equivalent” when they provide the same level of safety, which can reduce duplicate checks and delays.

But these provisions don’t remove all SPS barriers, as Indian authorities retain the final decision and assesses cases individually. At the same time, customs procedures become simpler, with greater use of electronic paperwork, faster processing and clearer appeal options if problems arise at the border. Services trade also benefits from improved market access and transparency, including fair treatment and easier recognition of professional qualifications.